Blurred lines: the EM’ification of DM

A shift in volatility in developed markets means asset allocators face a new reality.

Frontier markets sit within the broader emerging market (EM) debt universe, but are typically at an earlier stage of economic development, with less well-developed financial markets. In fact, frontier markets today resemble emerging markets in the early 2000s – high-growth economies, offering the potential for attractive risk-adjusted returns.

Compelling diversification characteristics have helped make the frontier market opportunity set highly relevant for asset allocators today. The liquid frontier universe spans almost 60 countries globally, and can be accessed through hard currency sovereign bonds, local currency bonds and FX markets. Each of these asset classes carries different liquidity, volatility and return characteristics. Hard currency debt offers access to a broader set of issuers and generally better liquidity1 as most hard currency issuance goes into global benchmarks, which have minimum liquidity requirements. By contrast, local markets can offer higher yields, lower volatility and a lower correlation to global indices, while providing direct exposure to diverse domestic reform and monetary-policy cycles – this makes the asset class a powerful diversifier for investment portfolios.

Today, the frontier market universe is bigger, broader and more liquid than ever, with secondary market activity having expanded alongside issuance and new country entrants. However, these markets remain less researched and less crowded than more developed emerging markets, resulting in significant alpha-capture potential.

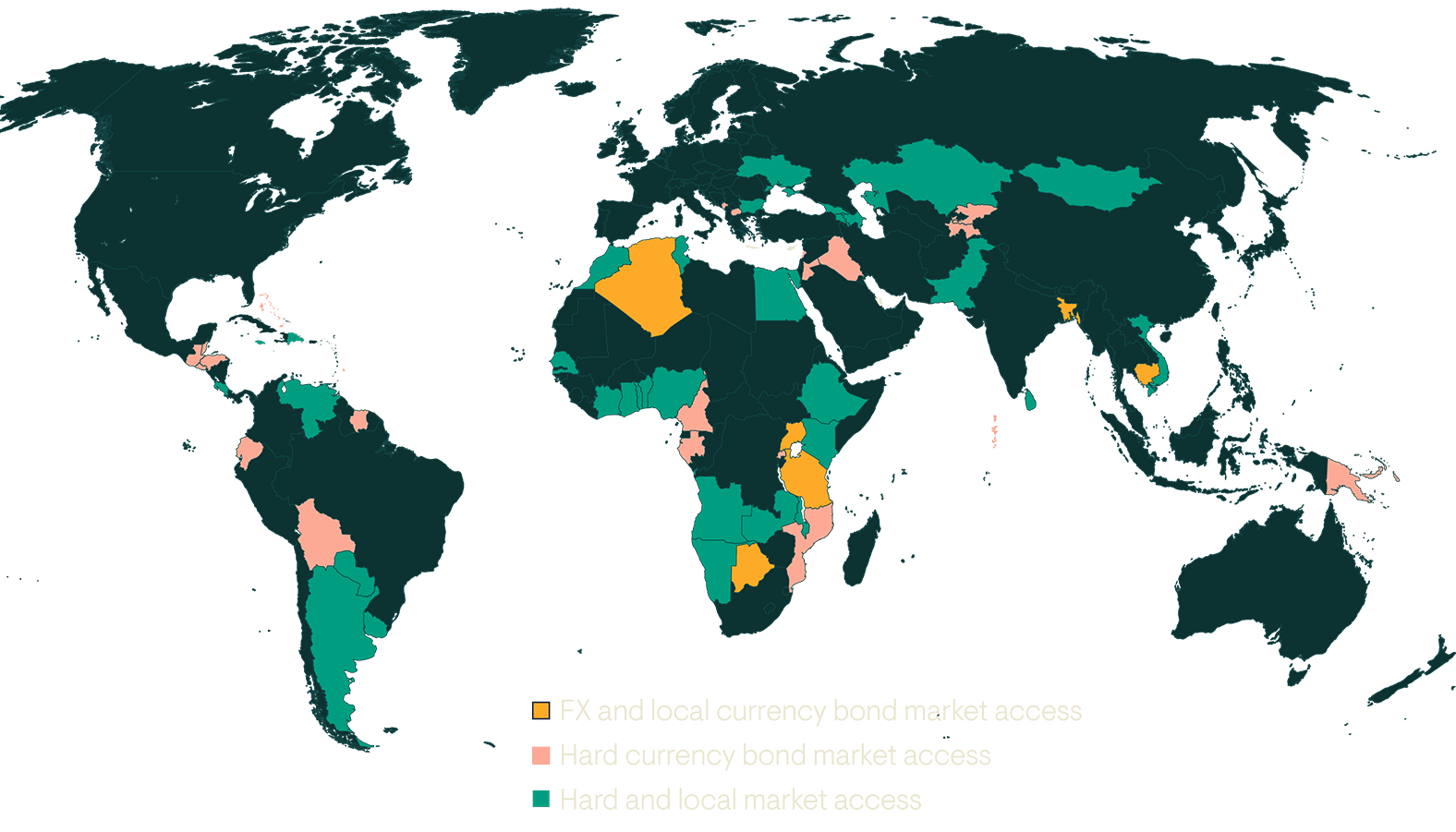

Figure 1: The liquid frontier market universe now comprises 58 countries, 35 NDF/deliverable FX markets, 28 local bond markets and 50 hard currency bond markets

Source: Ninety One, as at 31 December 2025. For an overview of asset class characteristics, please see the Appendix.

Frontier markets typically provide a significant yield pick-up over more mature emerging markets, as shown in Figure 2.

In part, this reflects market-development factors. Nascent domestic savings industries in frontier-market economies mean that demand for longer-dated assets (such as sovereign bonds) is less entrenched than in more developed markets – as a result, investors get higher compensation.

Figure 2: Compelling yields are on offer in frontier markets

Source: 30 April 2026, Bloomberg, Moody’s, Ninety One calculations.

The yield premium also reflects the structural challenges frontier markets face, which can make them more vulnerable to shock events. This was seen clearly in 2022, when fears over a global recession, combined with thinning liquidity and concerns over external indebtedness, weighed heavily on frontier markets, resulting in a ‘sudden stop’ in foreign investor flows. Crucially, indiscriminate market moves like this can create entry points for investors to gain exposure to economies where long-term structural improvements are being overlooked. However, careful navigation of this highly diverse investment universe is vital. Put simply, investors should favour countries that are willing and able to consolidate fiscal finances, even in the face of tighter financial conditions.

Frontier markets have particular challenges to overcome as they develop and reach their potential:

The key to frontier markets’ success is how they tackle these three challenges. Reforms should seek to increase revenue – broadening the tax base and reducing levels of informality – while also stabilising and lowering the interest costs of their debt. Egypt and Argentina have both been successful in recent years and have subsequently been rewarded with lower risk premia and credit rating upgrades.

Historically, local currency frontier debt has delivered lower absolute returns than hard currency debt, but a higher risk-adjusted return in reflection of relatively lower volatility, as shown in Figure 3. It has also shown smaller drawdowns than frontier hard currency debt and more mature emerging market local debt. One reason is that foreign participation is often low, benchmark representation is limited and capital tends to move more slowly. That tends to reduce sensitivity to the global bond market and can make diversified local allocations more resilient through the cycle.

Figure 3: A differentiated return and risk profile to global fixed income indices

Source: Bloomberg, Ninety One calculations, 30 April 2026. For further information on indices, please see Important information section.

A typical perception of frontier markets is that the underlying economies are on fragile footing. The reality is quite different. In recent years, frontier economies have emerged from the period of stress between 2020-2022 with stronger policy frameworks and improved fundamentals. Fiscal consolidation has generally been more pronounced than in many other sovereign bond markets. Across much of the universe, current accounts have improved and foreign-exchange reserves boosted.

Growth dynamics remain relatively strong across much of the frontier universe. Despite the shocks of the past decade, frontier economies have continued to show resilience, particularly outside of oil exporters. With war in the Middle East disrupting energy markets, economies’ commodity market exposure is a key concern for investors, with a risk-off shift causing a correction in frontier markets where investor positioning has become heavy over the past year. From a longer-term perspective, in the event of ongoing energy supply disruption resulting in a persistent rise in commodity prices, the likely impact will be even greater divergence in this already diverse investment universe. Markets that are relatively well positioned extend beyond oil exporters to include economies where oil is smaller in the import basket, and where inflation was benign before the conflict, such as many Latin American economies and South Africa.

From a structural perspective, asset class resilience is supported by more favourable demographic trends and scope for increased private-sector participation in many economies. Finally, the IMF remains a key anchor. IMF programmes continue to encourage policy discipline, transparency and reform follow-through, while multilateral support has helped reduce near-term funding pressure in a number of countries. That does not eliminate risk – frontier investing still requires selectivity. But risks today are increasingly localised rather than systemic, which improves the case for diversified, actively managed exposure.

Figure 4: Real GDP growth premia vs US

Figure 5: Debt to GDP

Source: IMF WEO April 2026, Ninety One calculations. For further information on indices, please see Important information section. Forecasts are inherently limited and are not a reliable indicator of future results.

Argentina illustrates how active investors can benefit from a frontier market that adopts a credible policymaking path. From being locked out of international capital markets following its default in 2020, Argentina’s turnaround has been one of the most compelling stories in the asset class. In short:

Nigeria’s reform journey over recent years has earned it credit rating upgrades and put its economy on a sustainable path, while providing a reform template for other high-yielding African markets.

There are significant benefits to investing across both the hard and local currency segments of the frontier market opportunity set as the performance of each sub-asset class is differentiated through the broader economic and monetary policy cycle. A blended portfolio provides the opportunity for alpha capture through: 1. top-down allocation between local and hard currency debt; and 2. bottom-up selection of the best assets in each market. In other words, a ‘blended’ allocation that provides access to multiple asset classes in a single portfolio may help balance different return drivers through the cycle.

More broadly, the inherent diversity of the frontier market opportunity set makes a highly selective investment approach vital. In our view, keys to successful investment outcomes include:

1. While local markets are typically less liquid, investability has improved steadily as more countries have opened their markets and settlement infrastructure has improved. For active investors, liquidity is no longer a valid reason for overlooking the asset class; it is one of the features that can create mispricing opportunities to exploit.

General risks. The value of investments, and any income generated from them, can fall as well as rise. Where charges are taken from capital, this may constrain future growth. Past performance is not a reliable indicator of future results. If any currency differs from the investor’s home currency, returns may increase or decrease as a result of currency fluctuations. Investment objectives and performance targets are subject to change and may not necessarily be achieved, losses may be made. Environmental, social or governance related risk events or factors, if they occur, could cause a negative impact on the value of investments.

Specific risks. Geographic/Sector: Investments may be primarily concentrated in specific countries, geographical regions and/or industry sectors. Currency exchange: Changes in the relative values of different currencies may adversely affect the value of investments and any related income. Default: There is a risk that the issuers of fixed income investments (e.g. bonds) may not be able to meet interest payments nor repay the money they have borrowed. The worse the credit quality of the issuer, the greater the risk of default and therefore investment loss. Emerging market: These markets carry a higher risk of financial loss than more developed markets as they may have less developed legal, political, economic or other systems.